COPYRIGHT NOTICE — This document is intended for internal use. It cannot be distributed to or reproduced by third parties without prior written permission from the Copyright Coordinator for the Office of the Auditor General of Canada. This includes email, fax, mail and hand delivery, or use of any other method of distribution or reproduction. CPA Canada Handbook sections and excerpts are reproduced herein for your non-commercial use with the permission of The Chartered Professional Accountants of Canada (“CPA Canada”). These may not be modified, copied or distributed in any form as this would infringe CPA Canada’s copyright. Reproduced, with permission, from the CPA Canada Handbook, The Chartered Professional Accountants of Canada, Toronto, Canada.

3031 Independence

Dec-2023

Overview

Engagement team members shall maintain and be seen to maintain independence and objectivity to fulfill the mandate of the Office.

This section outlines how team members, engagement leaders, and assistant auditors general all have an important role to play in achieving independence and ensuring threats to independence are managed through the application of appropriate safeguards.

OAG Policy

Office employees shall perform their duties and arrange their private affairs so that public confidence and trust in the integrity, independence, objectivity, and impartiality of the Office are protected. [Nov-2011]

Auditors, in particular, shall maintain and be seen to maintain independence and objectivity to fulfill the mandate of the Office. [Nov-2011]

Annually, the Office shall obtain written confirmation of compliance with its policies and procedures on independence from all Office personnel who, during the year, have met the definition of an engagement team member on an assurance engagement. [Nov-2011]

The Office shall promptly communicate identified breaches of independence policies and procedures to the engagement leader for resolution. [Nov-2011]

All individuals who meet the definition of an engagement team member, including internal and, where appropriate, external specialists, or who have been assigned to perform an engagement quality review, shall confirm their independence. [Dec-2022]

The engagement leader shall form a conclusion on team members’ compliance with independence requirements that apply to the assurance engagement. [Nov-2011]

The engagement leader shall identify threats to compliance with relevant ethical requirements and;

- evaluate the significance of those threats

- identify and apply safeguards to reduce threats to an acceptable level. [Dec-2023]

The engagement leader shall, throughout the engagement, remain alert to identify breaches of relevant ethical requirements by members of the engagement team and;

- evaluate the significance of the breach

- determine the impact of the breach on the assurance engagement

- determine the appropriate action to be taken [Dec-2023]

An assistant auditor general shall inform the engagement leader of any threats or breaches to independence that he or she becomes aware of. [Nov-2011]

OAG Guidance

Concept of independence

Independence is a fundamental principle for our Office and professionals performing assurance engagements. This principle is the foundation for public confidence in the reports our Office issues. It may be defined as the ability to act with integrity and objectivity and be seen to act this way.

The Office’s Code of Values, Ethics and Professional Conduct requires that all Office employees complete an annual Conflict of Interest Declaration form. This form includes an additional independence declaration for all individual working on assurance engagements. This annual process aids to ensure that our Office remains free of any influence which in the view of a reasonable observer would/could impair objectivity.

To perform an assurance engagement, practitioners need to observe and comply with relevant rules of professional conduct/codes of ethics applicable to the practice of public accounting issued by the various professional accounting bodies in Canada. In many of our engagements, the applicable rules are the CPA Code of Professional Conduct issued by the relevant provincial order. The CPA Code of Professional Conduct outlines the requirements for independence within Rule 204 Independence (“Rule 204” or “independence standard”). Rule 204 requires the Office or personnel performing an audit or assurance engagement to be and remain free of any influence, interest, or relationship which, impairs the professional judgment or objectivity.

Applicability at the engagement level

The CPA Code of Professional Conduct outlines the requirements for independence within Rule 204 Independence (“Rule 204” or “independence standard”). Rule 204 requires the persons on the engagement team or the firm (the Office) to be independent and has its own definition of an engagement team member. For purposes of determining who needs to be independent, engagement team member means:

- each member of the Office performing the assurance engagement;

- each contractor performing the assurance engagement, but does not include an external expert possessing skills, knowledge and experience in a field other than accounting or auditing whose work in that field is used to assist the member or Office in obtaining sufficient appropriate evidence;

- all other members of the Office who can directly influence the outcome of the assurance engagement, including;

- those who recommend the compensation of, or who provide direct supervisory, management or other oversight of, the assurance engagement leader in connection with the performance of the assurance engagement.

- those who provide consultation regarding technical or industry-specific issues, transactions or events for the engagement team; and

- those who provide quality management for the assurance engagement; and

- all other persons in the Office or external to the Office who can directly influence the outcome of the assurance engagement.

The engagement leader is required to form a conclusion on compliance with independence requirements and should apply professional judgment in assessing who meets the definition of an engagement team member and the extent to which individuals who are consulted or engaged or who provide advice on the engagement have a direct influence on the outcome of the assurance engagement.

In addition, the engagement leader should consider whether known relationships between Office employees who are not on the engagement team and the entity may also create threats to independence.

The Office considers breaches of these requirements to be a very serious matter. Employees who breach these requirements are subject to appropriate disciplinary action, up to and including termination of employment. For members of a provincial professional accounting body, the engagement leader could refer the issue to the institute/order or association.

Specialists

Refer to section Applicability at the engagement level above for the definition of engagement team member for purposes of determining who needs to be independent

Internal specialists involved in performing the assurance engagement or who provide formal advice in their area of specialization meet the definition of an engagement team member.

External specialists do not always meet the definition of an engagement team member.

External specialists meet the definition of an engagement team member if they possess skills, knowledge, and experience in accounting or auditing, and their work in that field is used to help the auditor obtain sufficient appropriate evidence.

External specialists who possess skills, knowledge, and experience in a field other than accounting or auditing and whose work in that field is used to help the auditor obtain sufficient appropriate evidence, do not meet the definition of an engagement team member.

An internal specialist or external specialist (in accounting or auditing) who will be involved in performing the assurance engagement (i.e. performing procedures that will give rise to audit evidence used by the engagement leader to form a conclusion) would meet the engagement team member definition.

An internal specialist or external specialist (in accounting or auditing) providing formal advice regarding technical subject matter or industry-specific subject matter issues, transactions, or events for the assurance team would meet the engagement team member definition.

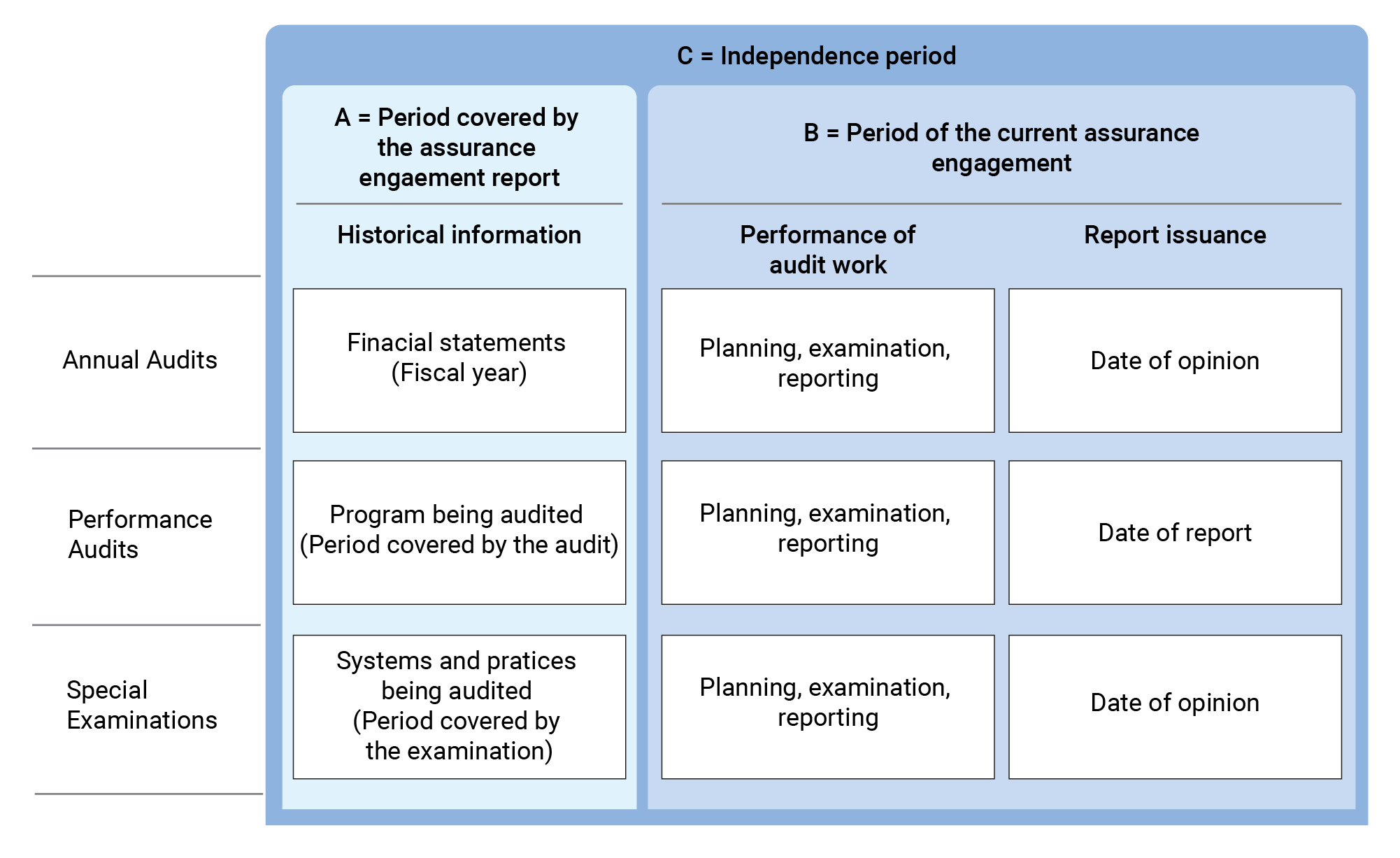

Independence period

The Office and those meeting the definition of engagement team members should be independent of the assurance entity during both the period covered by the assurance engagement report and the period of the current assurance engagement. This cumulative period starts at the beginning of the period covered by the assurance engagement report and ends when the assurance report is issued.

For further clarification, refer to Figure 1.1 below.

Figure 1.1 Independence period for each OAG product line

Process at the engagement level to comply with independence

The engagement leader must consider threats to independence throughout an assurance engagement. All individuals who meet the definition of an engagement team member, including internal and where appropriate, external specialists, or who have been assigned to perform an engagement quality review must perform the following for each assurance engagement they are involved in:

- Complete an Independence Confirmation.

- If no threats to independence are noted, provide the completed Independence Confirmation to the engagement leader for approval and inclusion in the audit file.

-

If a threat to independence is identified, an exception report is completed and the engagement leader proposes a resolution by applying the framework for resolution. The exception report should include a description of

(a) the nature of the engagement;

(b) the threat identified;

(c) the safeguard or safeguards identified and applied to eliminate the threat or reduce it to an acceptable level; and

(d) an explanation of how, in the senior personnel’s professional judgment, the safeguards eliminate the threat or reduce it to an acceptable level.

-

The engagement leader promptly communicates to the Internal Specialist, Values and Ethics, the safeguards and actions proposed to eliminate or reduce the threat.

-

The Internal Specialist, Values and Ethics, performs an objective review of the safeguards and actions proposed to eliminate or reduce the threat.

-

The engagement leader receives confirmation from the Internal Specialist, Values and Ethics, on the appropriateness of the proposed course of action, which may include proposed additional actions to reduce the threat to an acceptable level.

-

An individual should not commence work on the assurance engagement until any necessary safeguards to reduce or eliminate an identified threat to an acceptable level are in place.

-

The Internal Specialist, Values and Ethics may help ensure Records Management receives a copy of documentation for filing purposes.

The engagement leader ensures that evidence of compliance with independence requirements is documented.

If rotation is desirable but not practical for an individual engagement team member, the senior engagement personnel should consider how to address any associated risk. References to the Office’s policies and procedures regarding rotation should be considered. See OAG Audit 1071 Job Rotation.

The engagement leader, throughout the engagement, remains alert through observation and making inquiries as necessary, for breaches of independence requirements or the Office’s related policies or procedures by members of the engagement team. When new circumstances arise or information is obtained during the engagement that could result in an impairment of independence, team members must immediately report them to the engagement leader, who should make a decision as to whether work should stop immediately.

When joint audits are undertaken, the engagement leader should obtain assurance from the joint auditor that he or she has performed an independence assessment. Similarly, the Office should be in a position to provide the same assurance to the joint auditor.

If the engagement leader has an exception to disclose, the engagement leader should identify safeguards in cooperation with the Internal Specialist, Values and Ethics and sign the exception report. If an assistant auditor general has an exception to disclose, he or she should consult the engagement leader and Internal Specialist, Values and Ethics.

If an engagement quality reviewer identifies a threat to his or her independence or a threat to his or her ability to perform an objective review, he or she must immediately inform the engagement leader and the principal of methodology, Audit Services. See OAG Audit 3063 Engagement quality reviewer responsibilities.

Process at the Office level to comply with independence

Office employees complete an annual Conflict of Interest Declaration form, as required by and according to the OAG Code of Values, Ethics and Professional Conduct. This form includes an additional independence declaration for all staff working on audit engagements. Staff members who, during the course of the year, meet the definition of engagement team member on at least one assurance engagement are required to declare that they have read the Office policies on independence and that they comply with these policies and procedures, as required by relevant ethical requirements.

A conflict of interest is an incompatibility between an employee’s private interests and his or her duties as a public servant. A conflict of interest may arise from an interest, restriction, or relationship that, regarding an assurance engagement, would be seen by a reasonable observer to influence an employee’s judgment or objectivity in the conduct of the assurance engagement.

The Office has established conflict of interest measures that are included in the Code of Values, Ethics and Professional Conduct. These conflict of interest measures both protect Office employees from conflict of interest allegations and help them avoid situations of risk.

Office employees have the following overall responsibilities:

-

In carrying out their official duties, Office employees should arrange their private affairs in a manner that will prevent real, apparent, or potential conflicts of interest from arising.

-

If a conflict does arise between the private interests and the official duties of an employee, the conflict should be resolved in favour of the public interest.

Office employees also have the following specific duties:

-

They should not have private interests, other than those specifically permitted, that would be affected particularly or significantly by government actions in which they participate.

-

They should not solicit or accept transfers of economic benefit.

-

They should not place themselves in a position where they are under an obligation to any person who might benefit from special consideration or favour on their part or seek in any way to gain special treatment from them.

-

They should not step out of their official roles to assist private entities or persons in their dealings with the government where this would result in preferential treatment to the entities or persons.

-

They should not knowingly take advantage of, or benefit from, information that is obtained in the course of their official duties and that is not generally available to the public.

-

They should not directly or indirectly use, or allow the use of, government property of any kind, including property leased to the government, for anything other than officially approved activities.

An employee who does not comply with these requirements is subject to appropriate disciplinary action, up to and including termination of employment.

The annual Conflict of Interest Declaration form is designed to remind Office employees of the importance of the Office’s Code of Values, Ethics and Professional Conduct and the relevant ethical requirements, including independence. The form reinforces that Office employees and members of their immediate families should have no financial or other interests that could conflict with the employees’ responsibilities or call into question their judgment or objectivity.

Employees are obligated to submit a statement about their assets, liabilities, or other interests as set out in the Conflict of Interest Declaration form.

This obligation arises

- on commencing employment with the Office;

- annually thereafter; and

- when there is any change in an employee’s situation, including the acquisition or divestment of any reported interest.

Office employees must disclose all of their reportable assets, liabilities, or other interests (without indicating their value) that could jeopardize or call into question their judgment or objectivity. For purposes of the disclosure, other interests include personal relationships with staff or clients; gifts, hospitality (not allowable under the Code), or other benefits; or participation in outside employment or activities.

All employees complete the Conflict of Interest Declaration form and must declare that

- the statements made are true and complete;

- they have read and understand the OAG Code of Values, Ethics and Professional Conduct; and

- they commit to observing it in its entirety.

If, during the course of the year, an employee’s situation or circumstances change with respect to the declarations previously made, he or she is required to complete a new Conflict of Interest Declaration form and provide it immediately to the Internal Specialist Values and Ethics.

Assessing compliance with independence requirements

The Office expects engagement teams to apply a framework when assessing threats to independence. This framework requires the Office and its employees to

- identify threats to compliance with independence requirements;

- assess the significance of the threats identified;

- apply safeguards, when necessary, to eliminate or reduce the threat to an acceptable level; and

- document the threat and how safeguards eliminate or reduce it to an acceptable level.

Where safeguards are not available to reduce the threat or threats to an acceptable level, the engagement leader consults the Internal Specialist, Values and Ethics concerning eliminating the activity, interest, or relationship creating the threat or threats, or refusing to accept or continue the engagement, if possible, under applicable laws and regulations.

Identify threats to compliance with independence requirements. A threat to independence, for the purposes of this policy, is a situation, relationship, or circumstance that may give rise to a breach of an employee’s professional judgment or objectivity. When identifying threats to independence, care must be taken as threats are not always direct or overt and, in many cases, they can be quite subtle.

Threats to independence must be considered by all engagement team members throughout the assurance engagement. Threats to independence can be categorized into threats arising from self-interest, self-review, advocacy, familiarity, and intimidation. OAG Audit 1031 Ethical requirements relating to an assurance engagement discusses these categories of threats.

Evaluate the significance of identified threats. OAG Audit 1031 Ethical requirements relating to an assurance engagement discusses the factors to consider when assessing the significance of identified threats.

Apply safeguards, when necessary, to eliminate or reduce the threat to an acceptable level. Senior engagement personnel (engagement leader and assistant auditor general), evaluate the significance of identified threats.

Safeguards are necessary when identified threats are at a level where a reasonable observer would likely conclude that compliance with the relevant ethical requirements, including independence, may be compromised. OAG Audit 1031 Ethical requirements relating to an assurance engagement provides examples of safeguards that may eliminate or reduce identified threats to an acceptable level.

If a threat is other than insignificant, senior engagement personnel identify and apply available safeguards to eliminate or reduce the threat to an acceptable level. The Internal Specialist, Values and Ethics, objectively reviews the threat and safeguards.

Document the threat and how safeguards eliminate or reduce the threat to an acceptable level. The ongoing evaluation and disposition of threats to independence should be supported by evidence obtained both before accepting an engagement and while it is being performed. For each threat identified as other than insignificant, an engagement exception report is completed and the engagement leader ensures that all relevant decisions taken are supported and documented. Final exception reports are provided to Records Management for filing purposes. Exception reports are not placed in the audit file due to the personal and confidential nature of the content.

Breach to independence

There may be occasions when an employee or the Office is inadvertently in breach of the relevant ethical requirements, including independence.

Engagement personnel promptly notify the engagement leader of a breach to independence requirements.

If matters come to the engagement leader’s attention through the system of quality management or otherwise, that indicate that a member of the engagement team is in breach of the independence requirements, the engagement leader, in consultation with the Internal Specialist, Values and Ethics, will ensure to comply with Independence Rule 204.6 which sets out the requirements and processes for:

- reporting the issue within the Office,

- ensuring that the nature of the breach is analyzed and evaluated and that appropriate actions are taken,

- considering whether safeguards can be applied, and whether the assurance engagement may be continued or whether it should be terminated, and obtaining concurrence from client as appropriate,

- considering whether previously issued assurance reports should be withdrawn,

- reporting the matter to the entity’s audit committee or those charged with governance,

- documenting the analysis and conclusions, and

- reporting the matter to the provincial CPA body/Ordre.

Independence Rule 204.6 provides a requirement for the breach of Independence to be communicated in writing to the entity’s audit committee or those charged with governance and provides the framework for that communication.

The engagement leader documents the breach to independence in an exception report and promptly communicates a proposed action with the Internal Specialist, Values and Ethics. The engagement leader and the employee’s Principal (where different) receive confirmation from the Internal Specialist, Values and Ethics, on the appropriateness of the proposed actions. Records Management receives a copy of the final exception report for filing purposes.

Differences of opinion

If differences of opinion arise on the resolution of independence matters, team members should follow the procedures established in OAG Audit 3082 Resolution of differences of opinion.

Office employees are entitled to file a complaint or allegation if they believe the Office or its employees have failed to comply with professional standards, including relevant ethical requirements, regulatory and/or legal requirements, including the system of quality management, according to OAG Audit 1091 Complaints and allegations.

Referrals to the Internal Specialist, Values and Ethics

Independence matters that must be referred to the Internal Specialist, Values and Ethics, include

-

instances where specified actions and procedures will be necessary to appropriately manage threats and potential threats to independence, and

-

independence compliance concerns raised by Office personnel and/or members of the audit team.