Annual Audit Manual

COPYRIGHT NOTICE — This document is intended for internal use. It cannot be distributed to or reproduced by third parties without prior written permission from the Copyright Coordinator for the Office of the Auditor General of Canada. This includes email, fax, mail and hand delivery, or use of any other method of distribution or reproduction. CPA Canada Handbook sections and excerpts are reproduced herein for your non-commercial use with the permission of The Chartered Professional Accountants of Canada (“CPA Canada”). These may not be modified, copied or distributed in any form as this would infringe CPA Canada’s copyright. Reproduced, with permission, from the CPA Canada Handbook, The Chartered Professional Accountants of Canada, Toronto, Canada.

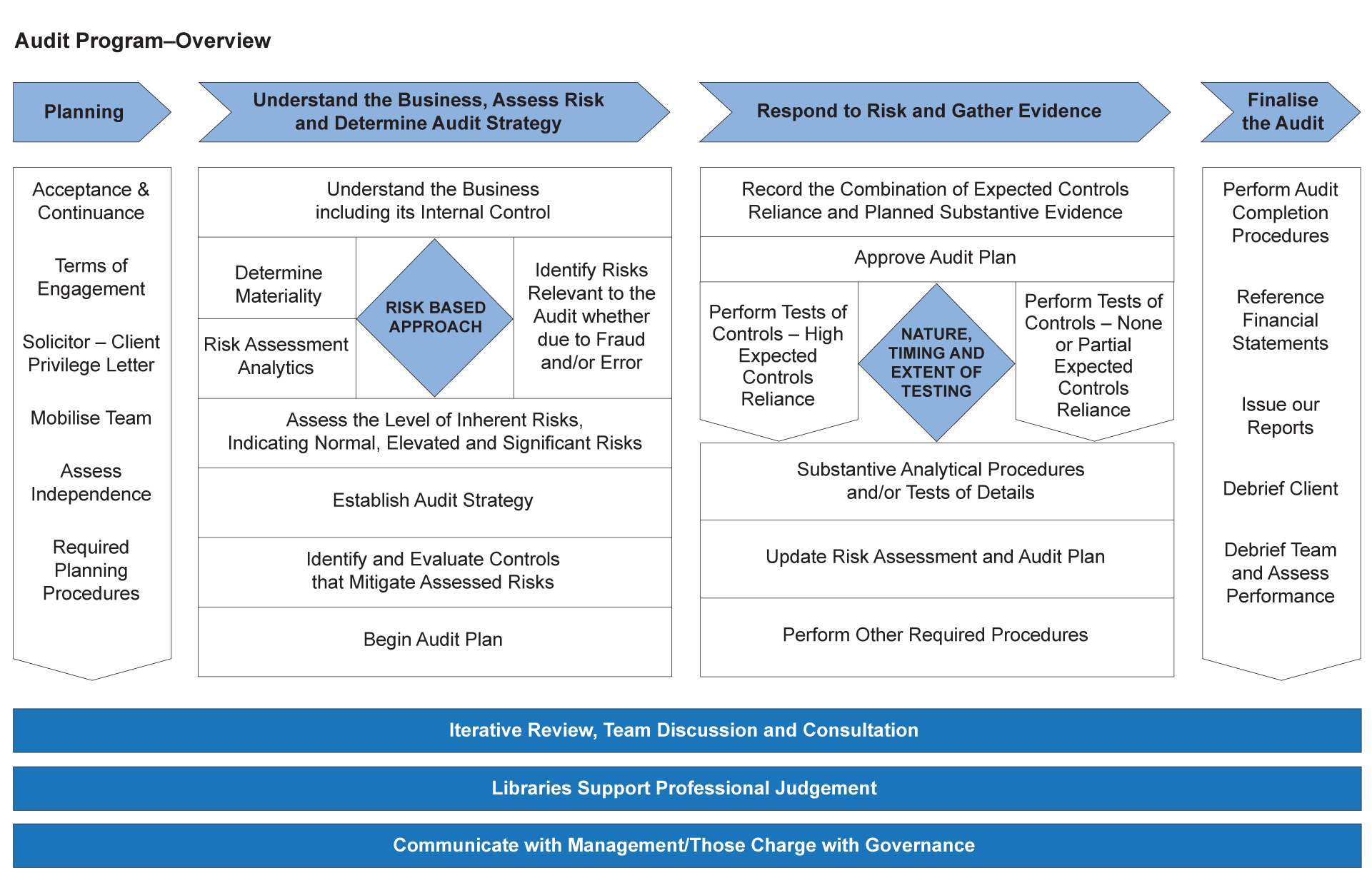

202 Audit Program—Overview

Oct-2012

In This Section

Audit program overview diagram

Overview

This topic explains:

- How the audit program is used to support an effective and efficient audit process

The following Overview diagram is designed to help you understand how the elements of OAG annual audit methodology fit together.

Audit program overview diagram

OAG Guidance

The Overview diagram below provides a high level illustration of the principal elements of the OAG annual audit methodology. The diagram shows our focus on a top-down risk-based approach and gives a high level representation of both the auditor's thought process and its practical application.