Annual Audit Manual

COPYRIGHT NOTICE — This document is intended for internal use. It cannot be distributed to or reproduced by third parties without prior written permission from the Copyright Coordinator for the Office of the Auditor General of Canada. This includes email, fax, mail and hand delivery, or use of any other method of distribution or reproduction. CPA Canada Handbook sections and excerpts are reproduced herein for your non-commercial use with the permission of The Chartered Professional Accountants of Canada (“CPA Canada”). These may not be modified, copied or distributed in any form as this would infringe CPA Canada’s copyright. Reproduced, with permission, from the CPA Canada Handbook, The Chartered Professional Accountants of Canada, Toronto, Canada.

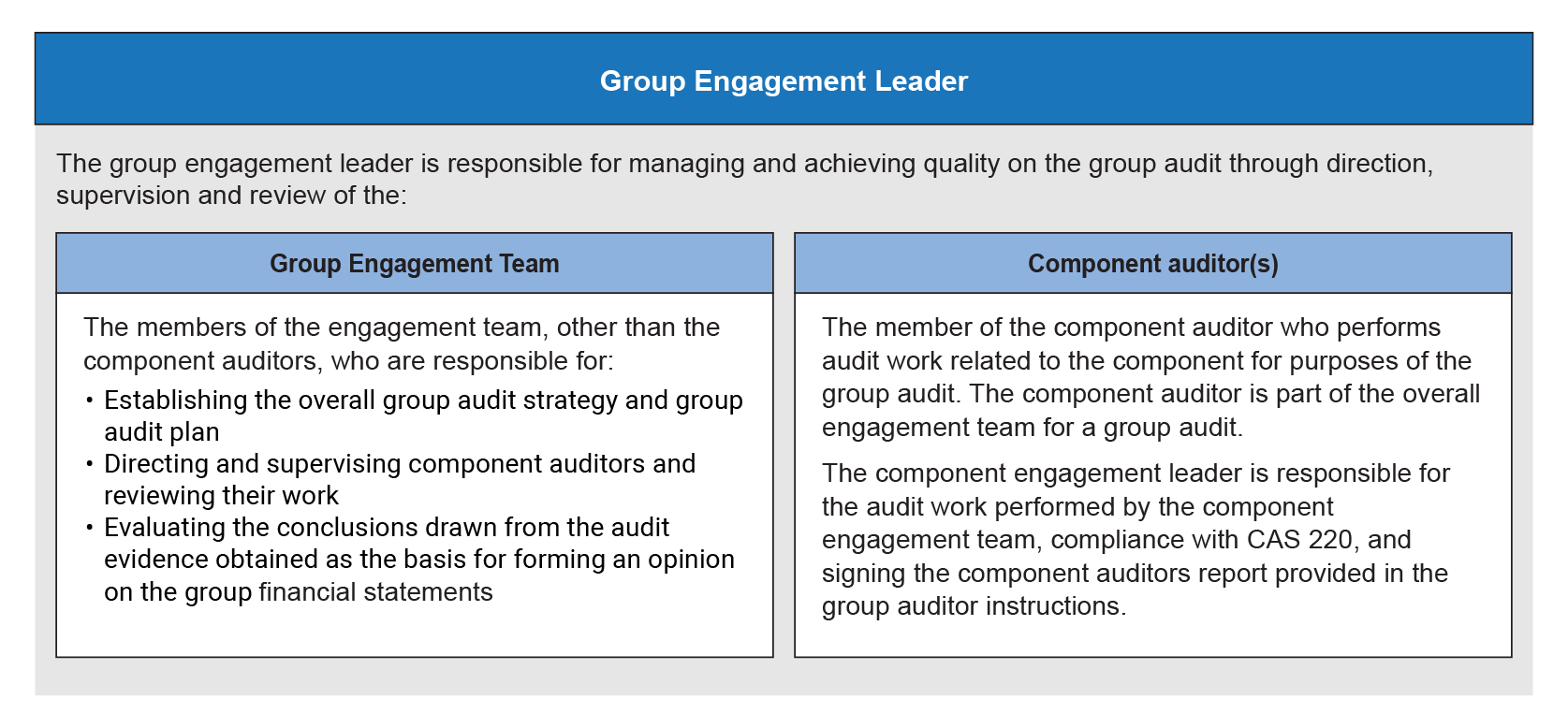

2312 Responsibilities of the group engagement leader

Dec-2023

In This Section

Managing and achieving quality on a group audit

Engagement leader’s review of the overall group audit strategy and plan

CAS Requirement

The engagement partner shall take overall responsibility for managing and achieving quality on the audit engagement, including taking responsibility for creating an environment for the engagement that emphasizes the firm's culture and expected behaviour of engagement team members. In doing so, the engagement partner shall be sufficiently and appropriately involved throughout the audit engagement such that the engagement partner has the basis for determining whether the significant judgments made, and the conclusions reached, are appropriate given the nature and circumstances of the engagement (CAS 220.13).

In creating the environment described in paragraph 13, the engagement partner shall take responsibility for clear, consistent and effective actions being taken that reflect the firm's commitment to quality and establish and communicate the expected behaviour of engagement team members, including emphasizing (CAS 220.14):

(a) That all engagement team members are responsible for contributing to the management and achievement of quality at the engagement level;

(b) The importance of professional ethics, values and attitudes to the members of the engagement team;

(c) The importance of open and robust communication within the engagement team, and supporting the ability of engagement team members to raise concerns without fear of reprisal; and

(d) The importance of each engagement team member exercising professional skepticism throughout the audit engagement.

If the engagement partner assigns the design or performance of procedures, tasks or actions related to a requirement of this CAS to other members of the engagement team to assist the engagement partner in complying with the requirements of this CAS, the engagement partner shall continue to take overall responsibility for managing and achieving quality on the audit engagement through direction and supervision of those members of the engagement team, and review of their work (CAS 220.15).

The group engagement partner is responsible for the direction, supervision and performance of the group audit engagement in compliance with professional standards and applicable legal and regulatory requirements, and whether the auditor’s report that is issued is appropriate in the circumstances. As a result, the auditor’s report on the group financial statements shall not refer to a component auditor, unless required by law or regulation to include such reference. If such reference is required by law or regulation, the auditor’s report shall indicate that the reference does not diminish the group engagement partner's or the group engagement partner's firm's responsibility for the group audit opinion (CAS 600.11).

CAS Guidance

The nature and extent of the actions of the engagement partner to demonstrate the firm’s commitment to quality may depend on a variety of factors including the size, structure, geographical dispersion and complexity of the firm and the engagement team, and the nature and circumstances of the audit engagement. With a smaller engagement team with few engagement team members, influencing the desired culture through direct interaction and conduct may be sufficient, whereas for a larger engagement team that is dispersed over many locations, more formal communications may be necessary (CAS 220.A30).

OAG Guidance

Group auditor responsibilities

Within the context of a group audit, the group engagement leader is the 'engagement partner' as described by CAS 220.C12(a) for the purpose of the group audit report, and, therefore, takes overall responsibility for managing and achieving quality on the group audit engagement through direction and supervision of the group engagement team and component auditors, and through review of their work. The group engagement leader needs to be sufficiently involved in the work of the group engagement team and component auditors throughout the group audit engagement to form the basis for determining that the significant judgments made, and conclusions reached are appropriate given the nature and circumstances of the engagement as required by CAS 220.40.

The group engagement leader complies with the requirements of OAG Audit 3062 as it relates to the group audit overall, and as adapted for the circumstances of a group audit. The group engagement leader evidence their sufficient and appropriate involvement throughout the group audit by, for example:

-

Communicating instructions to component auditors and reviewing the Acknowledgment of Receipt obtained from the component auditor(s). Clear and timely communication between the group engagement team and the component auditors about their respective responsibilities, along with clear direction to the component auditors about the nature, timing and extent of the work to be performed and the matters expected to be communicated to the group engagement team, helps establish the basis for effective two-way communication. Refer to OAG Audit 2340 for further guidance.

-

Participating in team planning meeting(s). Although team planning meeting(s) occur during the planning phase of the engagement, a significant number of planning activities are commonly undertaken in advance of the team planning meeting(s), and the team planning meeting(s) is where the group engagement leader and team manager and component engagement leader and team manager convey those plans to the rest of the group engagement team and component auditors for their understanding, input, discussion and agreement. Refer to OAG Audit 2330 for further guidance.

-

Participating in team discussions/taking stock meetings throughout the group audit engagement. "Taking stock" meetings facilitate direction and supervision of the group engagement team members and component auditors by the group engagement leader, team manager and more experienced engagement team members and provide some of the evidence of the group engagement leader's fulfillment of the CAS 220.30 requirement. It also provides an opportunity for the group engagement leader to be involved throughout the group audit in order to manage and achieve audit quality. Refer to OAG Audit 2342 for further guidance.

-

Performing component auditor visits (see OAG Audit 2340.1).

-

Reviewing the work performed by the component auditor(s) remotely or on site as part of a visit to the component auditor's location (see OAG Audit 2361).

The nature, timing and extent of direction and supervision of component auditors and review of their work may be tailored based on the nature and circumstances of the engagement, including, for example:

-

The assessed risks of material misstatement (e.g., if the group engagement team has identified a significant risk for the group audit relevant to the work of the component auditor, the group engagement team's direction and supervision of the component auditor's work is focused on the significant risk area and may be less extensive for other areas).

-

The competence and capabilities of the component auditors performing the audit work (e.g., if the group engagement team has no previous experience working with a component auditor, the group engagement team may communicate more detailed instructions, increase the frequency of discussions or other interactions with the component auditor, or assign more experienced individuals to oversee the component auditor as the work is performed).

-

The location of engagement team members, including the extent to which engagement team members are dispersed across multiple locations.

-

Access to the component auditor's audit documentation (e.g., when law or regulation precludes component auditor audit documentation from being transferred out of the component auditor's jurisdiction, the group engagement team may be able to review the audit documentation at the component auditor's location or remotely through the use of technology) (see OAG Audit 2321).

Component auditor responsibilities

The component engagement leader is considered the 'engagement partner' as described by CAS 220.C12(a) for the purpose of the work performed by the component engagement team. Therefore, the component engagement leader takes responsibility for managing and achieving quality on the work performed by the component engagement team through direction and supervision of the component engagement team and review of their work. The component engagement leader follows OAG Audit 3062 as it relates to the work performed by the component engagement team.

CAS Requirement

The group engagement partner shall review the overall group audit strategy and group audit plan (CAS 600.16).

The auditor shall develop an audit plan that shall include a description of (CAS 300.9):

(a) The nature, timing and extent of the planned direction and supervision of engagement team members and the review of their work.

(b) The nature, timing and extent of planned risk assessment procedures, as determined under CAS 315.

(c) The nature, timing and extent of planned further audit procedures at the assertion level, as determined under CAS 330.

(d) Other planned audit procedures that are required to be carried out so that the engagement complies with CASs.

The engagement partner shall determine that the nature, timing and extent of direction, supervision and review is planned and performed in accordance with the firm's policies or procedures, professional standards and applicable legal and regulatory requirements (CAS 220.30(a)).

CAS Guidance

The group engagement partner's review of the overall group audit strategy and group audit plan is an important part of fulfilling the group engagement partner's responsibility for the direction of the group audit engagement (CAS 600.A22).

OAG Guidance

The planning Sign-off procedure requires the team manager and engagement leader to affirm that the overall audit strategy and detailed audit plan (including group audit considerations, where applicable), are responsive to the assessed risks of material misstatement. In a group audit situation, this means that the group engagement team has:

-

Performed appropriate risk assessment procedures at the group level, and significant and/ or elevated risks have been identified.

-

Determined appropriate materiality levels to be applied by the group engagement team and component auditors.

-

Determined, in respect of significant FSLIs and not significant but material FSLIs, the testing strategy.

-

Determined the type of work to be performed on the financial information of components.

-

Determined, for significant and elevated risks, the planned audit response to address these risks and communicated this information (or planned to communicate this information) to component auditors.

-

Communicated to component auditors their responsibility to perform their work in accordance with CAS, or other GAAS (as relevant).

-

Determined that the nature, timing and extent of the direction and supervision of the component auditors and review of their work has been planned. CAS 220 requires that the engagement leader determines that the nature, timing and extent of direction and supervision of engagement team members and the review of their work is appropriately planned. Further, CAS 300 requires that our audit plan includes a description of the planned direction and supervision of engagement team members, and the review of their work.

-

Communicated relevant information to component auditors (e.g., through the Letter of Instructions for Use on Group Audits).

The engagement leader's review of the overall group audit strategy may be evidenced in different ways, including:

-

The group engagement leader's review of the interoffice letter of instructions that communicated information about the overall group audit strategy and audit plan to component auditors.

-

Discussions, supported by appropriate documentation, at meetings (e.g., team planning meeting(s)) held between the group engagement team and component auditors.

-

The group engagement leader's review of the group engagement team's documentation related to the audit strategy and plan.