Performance Audit Manual

COPYRIGHT NOTICE — This document is intended for internal use. It cannot be distributed to or reproduced by third parties without prior written permission from the Copyright Coordinator for the Office of the Auditor General of Canada. This includes email, fax, mail and hand delivery, or use of any other method of distribution or reproduction. CPA Canada Handbook sections and excerpts are reproduced herein for your non-commercial use with the permission of The Chartered Professional Accountants of Canada (“CPA Canada”). These may not be modified, copied or distributed in any form as this would infringe CPA Canada’s copyright. Reproduced, with permission, from the CPA Canada Handbook, The Chartered Professional Accountants of Canada, Toronto, Canada.

6040 Selection of Items for Review

May-2024

Overview

The objective of the engagement teams when selecting items for review is to obtain sufficient and appropriate evidence to conclude against the audit objective.

OAG Policy

When representative sampling is used in a reasonable assurance engagement, at a minimum, audit samples shall be sufficient to attain a confidence interval of 10% and a confidence level of 90%. Sampling for audits of high risk or sensitivity shall be sufficient to attain the confidence interval of 5% and confidence level of 95%. [Jul-2019].

OAG Guidance

When planning and conducting a direct engagement, engagement teams are required to obtain sufficient and appropriate evidence on which to base audit conclusions.

Selection of items for review

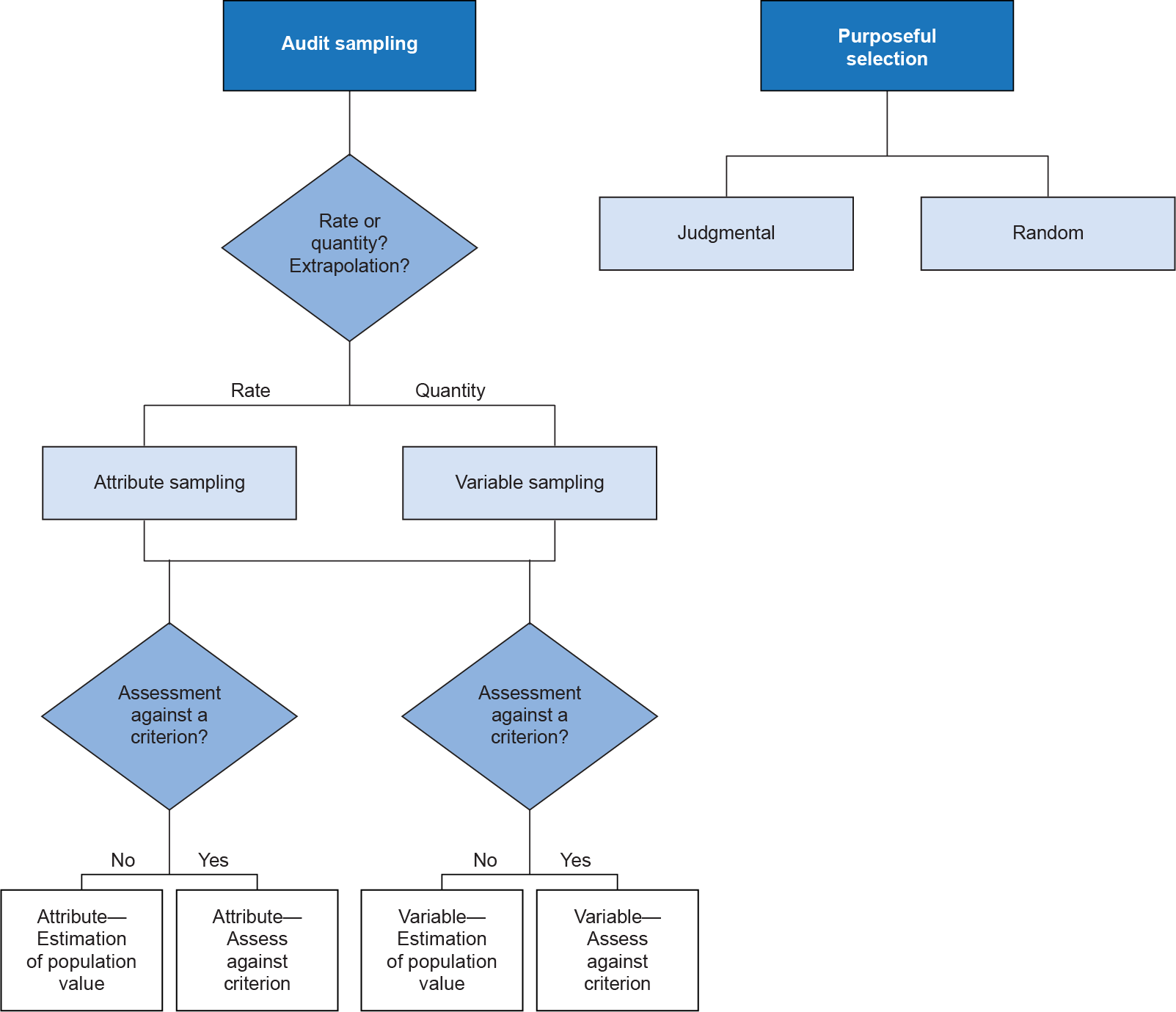

Engagement teams can rarely examine an entire population of items, which necessitates their review of just a selection. The 2 fundamental types of selection are audit sampling and purposeful selection.

Exhibit 1—Types of selection

| Selection type | Definition | Purpose |

|---|---|---|

|

Audit sampling Also referred to as representative sampling or generalizable sampling |

Audit sampling is the application of auditing procedures to a representative group of less than 100% of the items within a population of audit relevance such that all sampling units have a chance of selection in order to provide the auditor with a reasonable basis on which to draw conclusions about the entire population. |

Conclude on the overall population of items. |

|

Purposeful selection Also referred to as targeted testing |

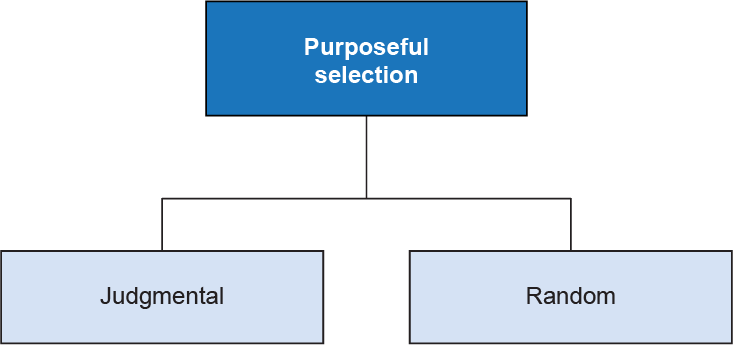

Purposeful selection is used to comment or conclude specifically on the items chosen for examination. There are 2 ways to select items: judgmental selection and random selection. |

Conclude specifically on the items selected. Purposeful selection has no statistical basis for concluding on an entire population of items. |

Engagement teams need sampling or selection plans whenever an audit procedure is designed to include audit sampling or purposeful selection.

Questions to consider when building a sampling or selection plan

If your team is considering selecting items to review, see below for a list of questions your team should consider.

Exhibit 2—Questions to consider for selection plan

| Consideration | Question |

|---|---|

|

Purpose of the selection or sample |

|

|

Population characteristics |

|

Framework for selecting items for review

The following chart provides a framework describing the types of item selection.

Exhibit 3—Framework for audit sampling and purposeful selection

Audit sampling

Audit sampling should be considered in the following circumstances:

- There is a well-defined population that is relevant to the audit.

- It is impractical to examine the entire population.

- The population is accessible.

- The representation of that population is reliable (that is, accurate and complete).

- The team has the audit resources it needs.

Audit sampling is very efficient with medium and large populations, but it can be inefficient for small populations. If teams are considering audit sampling with populations of less than 100, they should consult with the OAG Internal Specialist, Research and Quantitative Analysis.

Confidence interval and confidence level

The OAG’s policy is that all audit sampling should be performed with a confidence level of 90% or above and a confidence interval of 10% or below based on the assessed risk of significant deviation from the applicable criteria used to measure or evaluate the audit objectives. The engagement team shall consider higher confidence levels and more precise confidence intervals when the risk of significant deviation from the applicable criteria is assessed to be high.

Two measures inform about how effective a sample is likely to be as an estimator of a population: confidence interval and confidence level.

The confidence interval (also known as the margin of error) is the range of values with which the engagement team can be reasonably confident that the true population value resides, given the result from the sample. Smaller, or narrower, confidence intervals mean that there is greater precision around the estimate of a population. For example, the narrower confidence interval of +/-5 is more precise than the wider confidence interval of +/-10. In the first case, the engagement team may be confident that the true population value lies from 5 below the sample value to 5 above it. In the second case, the team would be confident only that the population value rests within the interval from 10 below the sample value to 10 above it, a much wider range. This wider range means that the confidence interval is less precise.

The confidence level is a statistical measure of the confidence that the true population value is within the specified confidence interval. The confidence level does not relate to the sample value. It relates to the confidence interval for the sample value.

Confidence level and confidence interval are closely interrelated, and both help to determine what the sample size should be. We typically compute our sample sizes so that we achieve particular targets for confidence interval and confidence level. Per our policy, when audit sampling is used, at a minimum, audit samples shall be sufficient to attain a confidence interval of 10% and a confidence level of 90%. Sampling for audits of high risk or sensitivity shall be sufficient to attain the confidence interval of 5% and confidence level of 95%.

So, given a sample value of 30% non-compliance, we might say that we are 90% confident that the true population value is between 10 less (20%) and 10 more (40%) using the OAG’s minimum requirements.

Expected error and tolerable error

Expected error is the best estimate of the error or deviation that exists in a population. Tolerable error is the criterion against which we are assessing the error or deviation we find. For example, if an entity has a performance standard that no more than 20% of transactions take longer than a target of 5 days, then the tolerable error would be 20 Teams might then look at prior years as a guide to expected error. For example, if the average percentage of transactions exceeding 5 days for the past 3 years was 5%, then teams might take 5% as an estimate of expected error. If, however, volume had sharply increased or processing had become more complex, teams might increase the expected error to account for these changes. As the expected error increases to approach the tolerable error, sample sizes can become very large. However, if teams underestimate expected error, they will need to go back and extend their sample, as the sample is then not sufficient in size to assess the population.

Types of audit sampling

There are 2 types of audit sampling: attribute sampling and variables sampling. Attribute sampling is the sampling approach most commonly used by direct engagement teams; variables sampling is more commonly used for financial audits.

Exhibit 4—Considerations for each type of sampling

| Consideration | Attribute sampling | Variables sampling |

|---|---|---|

|

Purpose |

Assess the proportion of an attribute of interest to the auditor. |

Extrapolate amounts or quantities. |

|

Use |

Can be used for both direct engagements and financial audit. |

Most often used for financial audit. |

|

Example |

An attribute might be whether transactions are in error or not in error, whether individuals are male or female, whether offices are open or closed, or whether a control procedure was done properly or not. |

The amount of error in salary among employees of the OAG. |

|

Suitability |

Not suitable for the extrapolation of amounts, such as dollars in error. |

Not suitable for the extrapolation of the proportion of items in error. |

|

Information needed |

If assessing against a criterion, the following information is also needed:

|

If assessing against a criterion, the following information is also needed:

|

|

Sample size |

Note that sample sizes are the largest when the attribute split is roughly 50%-50%. |

|

|

Common methods to assess against a criterion value |

Regularly used for special examinations and financial audits. Can be used for direct engagements. Normally, controls testing and accept-reject testing are used when the expected error is 0 or very low. See the OAG Audit 6050 in the Annual Audit Manual for more information on controls testing and 7043 for accept-reject testing. |

Regularly used in financial audits. Can increase the efficiency of variables sampling. Can be used for direct engagements. See OAG Audit 7044.2 in the Annual Audit Manual for more information on dollar unit sampling and OAG Audit 7044.1 for non-statistical sampling. |

Sample size for items to be selected for review

Two common methods of attribute sampling are presented in the above table: Controls testing and accept-reject testing. References to the annual audit manuals are relevant except for the tables to help engagement teams identify the sample sizes for direct engagement.

Controls testing

Direct engagement sample sizes for controls testing slightly differ from those used in OAG Audit 6053 in the Annual Audit Manual. In order to obtain a high level of assurance, the sample sizes when testing a control are presented in the table below.

Exhibit 5—Sample sizes for high levels of assurance

| Frequency of control | Assumed population of controls | Number of items to test for a high level of assurance at 90% confidence level | Number of items to test for a high level of assurance at 95% confidence level |

|---|---|---|---|

|

Annual |

1 |

1 |

1 |

|

Quarterly |

4 |

2 |

2 |

|

Monthly |

12 |

2 |

5 |

|

Weekly |

52 |

5 |

15 |

|

Daily |

250 |

20 |

40 |

|

Multiple times per day |

More than 250 |

25 |

60 |

Accept-reject testing

Direct engagement sample sizes for accept-reject testing differ greatly from those used in OAG Audit 7043.1 and are presented below.

Exhibit 6—Number of items to test for high levels of assurance

| Desired level of assurance | Number of items to test for 0 exceptions tolerated | Number of items to test for 1 exception tolerated | Number of items to test for 2 exceptions tolerated |

|---|---|---|---|

|

High level of assurance (90%, 95%) |

25, 60 |

40, 95 |

55, 135 |

Engagement teams can consult the OAG Internal Specialist, Research and Quantitative Analysis, to confirm the sampling approach when needed.

The Annual Audit Manual also includes useful information in section OAG Audit 6052 Nature of controls tests and in section OAG Audit 7043.1 A five step approach to performing accept-reject testing. While not directly applicable to direct engagements, engagement teams can consult those sections to deepen their knowledge and understanding of the nature of controls tests and the accept-reject testing.

Application of sampling methods

Both attribute and variables sampling can be applied in 2 ways: to estimate a population value or to assess against a criterion.

Exhibit 7—Descriptions and examples of application

| Consideration | Estimate a population value | Assess against a criterion |

|---|---|---|

|

Purpose |

Intended to project the extent of error or deviation observed in the sample as an estimate of the population error or deviation. For example:

|

Intended to assess whether errors or deviations in the population exceeded a specified criterion value. For example:

It may not be appropriate to project the extent of error or deviation observed in the sample as an estimate of the population error or deviation. Teams should consult the data analytics and research methods team to learn about this option. |

|

Example |

Estimating the proportion of employees with errors in salary payments (attribute sampling) or the amount of error in salary payments (variables sampling). |

Assessing whether the proportion of employees with errors in salary exceeds 10% (attribute sampling) or whether the amount of error in salary payment exceeds $500 million (variables sampling). |

|

Use |

Used for direct engagements and financial audits. |

Sampling to assess against a criterion may provide efficiencies in performance audit. This sampling is most often used for special examinations and financial audits |

Purposeful selection

Purposeful selection is used to comment or conclude specifically on the items chosen for examination. Engagement teams performing direct engagements often encounter situations that are more amenable to purposeful selection, not audit sampling. This may be because significant portions of those populations are inaccessible to the audit, or the populations consist of many distinct smaller sub-populations. Also, the systems and processes and the controls that are applied to items in these 2 groups may be entirely different.

Exhibit 8—Types of purposeful selection

There are 2 types of purposeful selection: judgmental sampling and random sampling. Direct engagement teams often use a combined approach.

- Judgmental sampling relies on specific criteria that the team uses to select individual items for examination or to scope particular types of items for possible selection.

- Random selection is used when we do not have a particular approach in mind. Often, judgmental selection is used to define a particular set for potential examination, and then random selection is used to choose the items for examination.

A combined approach might alternate selections between a random item and the remaining highest-value item until all items have been selected.

Note: Engagement teams cannot extrapolate their findings to the overall population. Often, items are selected and examined as case studies, allowing auditors to focus on the particular aspects of each item that made it noteworthy for selection.

Documenting your sampling plan

Engagement teams document their detailed sampling plan including

- a statement about what the evidence will allow the engagement team to report

- the desired accuracy of the results

- the population size

- the size of the set of items or sample

- the selection or sampling criteria