COPYRIGHT NOTICE — This document is intended for internal use. It cannot be distributed to or reproduced by third parties without prior written permission from the Copyright Coordinator for the Office of the Auditor General of Canada. This includes email, fax, mail and hand delivery, or use of any other method of distribution or reproduction. CPA Canada Handbook sections and excerpts are reproduced herein for your non-commercial use with the permission of The Chartered Professional Accountants of Canada (“CPA Canada”). These may not be modified, copied or distributed in any form as this would infringe CPA Canada’s copyright. Reproduced, with permission, from the CPA Canada Handbook, The Chartered Professional Accountants of Canada, Toronto, Canada.

3082 Resolution of differences of opinion

Dec-2022

Overview

Differences of opinion arising during an assurance engagement shall be identified and resolved in a timely manner. The nature and scope of the difference of opinion, and resulting conclusions, are to be documented and implemented. An assurance engagement report is not dated until all differences of opinion have been resolved.

This section outlines the Office’s policies and procedures for dealing with and resolving differences of opinion within the engagement team, with those performing activities within the Office’s system of quality management, including those consulted, and, where applicable, between the engagement leader and the engagement quality reviewer.

OAG Policy

Differences of opinion shall be identified and resolved in a timely manner in accordance with the Office’s resolution process. [Nov-2011]

An assurance engagement report shall not be dated until all differences of opinion have been resolved. [Nov-2011]

The engagement leader shall ensure that the parties consulted during the resolution process are provided with all relevant facts and any previous consultative advice received. [Nov-2011]

The engagement leader shall ensure that the nature and scope of the difference of opinion and resulting conclusions are documented and implemented. [Nov-2011]

OAG Guidance

Differences of opinion

There may be times when significant disagreements arise within the engagement team, with those performing activities within the Office’s system of quality management, including those consulted (e.g., internal specialists) or between the engagement leader and the engagement quality reviewer. The process for resolving differences of opinion requires consultation between individuals who have the appropriate knowledge, seniority, and experience regarding the technical, ethical, and other issues involved.

Each professional staff member of the Office has the right and obligation to form his or her own conclusions on the significant matters arising from the areas of the engagement for which he or she is responsible, and for ensuring those views receive adequate consideration.

The assurance engagement team comprises professionals with varying levels of experience and expertise, and differences in opinion between members may arise. These differences, particularly those involving personnel at senior levels, generally involve highly judgmental and technical questions. In these cases, the matter is resolved and documented according to OAG Audit 1142 Evaluating, resolving, and communicating significant matters. If the matter is not deemed significant, the rationale for the decision is nevertheless documented in the engagement file to record the reasons for the selection of a particular outcome over a different outcome, where this is necessary to understand the conclusion reached.

Areas where differences of opinion may be more likely to arise include

-

selection of audit scope (what to audit), for example, what systems and practices comprise the scope of a special examination, or what the period of the audit will be;

-

criteria/best practice for performance audits and special examinations, including changes to OAG recommended criteria applied in special examinations;

-

selection and application of accounting principles;

-

evaluating estimated amounts in financial statements;

-

financial statement presentation and disclosure;

-

reporting and compliance, including our association with other information in documents containing the audited financial statements;

-

interpretation of authoritative pronouncements, both Office and professional;

-

interpretation of laws and regulations;

-

the nature, timing, and extent of auditing procedures;

-

circumstances resulting in a departure from a standard, unmodified engagement report, or standard for any management responses included in the report;

-

decisions around the overall negative or positive conclusion in a direct reporting engagement;

-

ethical and/or professional conduct issues; and/or

-

engagement review, quality review, and other quality assurance processes.

The engagement leader strives to identify differences of opinion as early as possible and address them on a timely basis. An assurance report cannot be dated until all differences of opinion have been resolved. At the end of each phase of the engagement (planning, examination, and reporting), the engagement leader should identify any differences of opinion and initiate resolution in a timely manner.

Disagreements involve people and personalities, and dispute resolution is not an area that can be completely addressed with specific policies and procedures.

Key success factors for dealing with differences of opinion to arrive at a satisfactory resolution are the following:

-

Ensure everyone involved has all the facts, knowledge, and technical skill to form professional opinions on the subject matter in dispute.

-

Differences should always be dealt with as soon as they arise. It is not acceptable to defer resolution to a later date.

-

Disagreements can arise from simple miscommunications that can be quickly rectified. Both sides should listen carefully to the other’s point of view. This is best achieved in a face-to-face meeting where each person presents his or her views.

-

Try to reach consensus.

Guiding principles for the Office’s resolution process are:

-

Informal and formal consultation on complex matters and matters of significance is encouraged. From time to time, formal consultation may result in a difference of opinion that shall be resolved on a timely basis and prior to dating the auditor’s report.

-

It is generally expected that disagreements are normally resolved by direct settlement.

-

It is inappropriate for the engagement leader to assume sole authority for resolving disagreements with parties consulted or a quality reviewer. A firm/Office process for resolving disagreements must be in place.

-

Resolution of differences of opinion must occur on a timely basis. The process must not be a barrier to timely resolution of issues.

-

A prerequisite to an effective resolution process is the objectivity of any individuals arbitrating and appealing the resolution.

-

The parties involved in arbitrating or appealing the matter MUST have a clear understanding of the relevant facts, an appropriate level of professional judgment, and collectively possess the corporate knowledge1 to form opinions on the subject matter in dispute.

-

Documentation of first, the issue and secondly, the agreed resolution is the responsibility of the audit team and a required component of the resolution process. It shall be agreed upon prior to concluding the matter is resolved.

-

The process should work for all forms of assurance engagements in the Office or an equivalent process shall exist for all product lines.

-

An individual assistant auditor general should have no involvement in direct settlement with the party consulted. This limitation is not intended to limit the ability of the parties involved to consult other individuals within the Office as they seek to finalize their views on a matter before concluding whether a disagreement exists. There may be significant value and insight provided by consulting others who may be able to quickly identify precedents, conflicting conclusions, or comparable situations that will help resolve the disagreement. An assistant auditor general consulted in such a situation should be careful not to express a view, but rather, provide input. Parties consulted shall recognize that such involvement may threaten their objectivity and resulting ability to arbitrate or appeal the disagreement.

-

An individual assistant auditor general taking decisions on behalf of or in place of the engagement leader effectively assumes the role of engagement leader and all of its associated responsibilities.

Documentation

The engagement leader ensures at a minimum that the resolution of the difference is documented in the engagement file. The Differences of Opinion template would normally be used to ensure the completeness of documentation. It is designed to capture

- the nature of the difference of opinion,

- alternative positions proposed along with their rationale,

- the names of successive persons consulted and their opinions,

- the conclusion reached and the rationale for it, and

- the steps taken to implement the conclusion reached.

Direct Engagements

For direct engagements, the engagement team collaborates with the Office’s most senior executives throughout the engagement process including the assistant auditors general of the practice and the Auditor General. Differences of opinion escalating beyond direct settlement may be subject to arbitration with senior executives who have not been part of direct settlement. The Auditor General has the ultimate authority in the final conclusions taken and constitutes final appeal.

For more information concerning the process of direct settlement, refer to the Annual Audit discussion below.

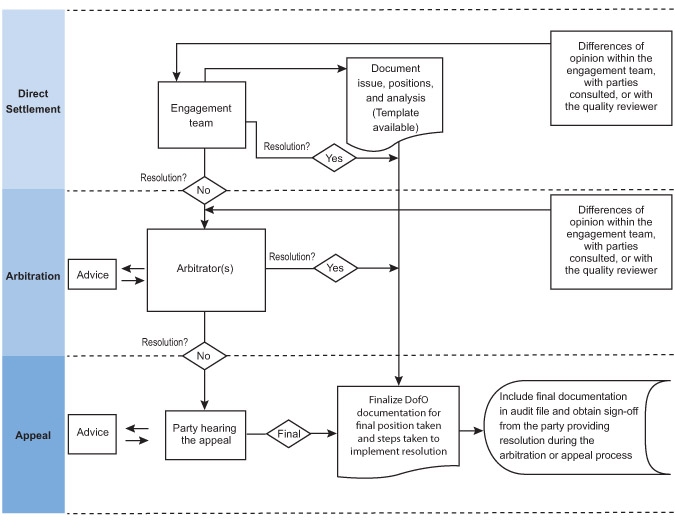

A flowchart of the principle activities involved in resolving a difference of opinion is presented at figure 1.1.

Annual Audits

To help all parties reach agreement, differences of opinion should be addressed on a timely basis following the steps outlined below. Note that the resolution process may be completed at any point if all parties agree with the proposed resolution.

If the party raising a difference of opinion is willing to allow the report signatory, other than the Auditor General, to make the final conclusion, the matter is not considered a difference of opinion requiring the use of this resolution process.

A difference of opinion shall be resolved following the three-step resolution process:

- Direct settlement

- Arbitration

- Appeal

If the parties involved conclude that the Auditor General shall make the final decision, this may imply they are in the appeal process. The parties involved typically shall not move into the appeal process without having received a decision from the arbitration process.

Step 1—Direct Settlement

Normally, disagreements are resolved directly. This may include discussion, research, and consultation with other knowledgeable parties. Most disagreements arise from simple miscommunications that can be quickly rectified. The engagement leader typically resolves differences of opinion within the team or with parties consulted (e.g., internal specialists).

Differences of opinion within the engagement team or with those consulted. If a difference of opinion arises within the engagement team or with those consulted, team members first discuss the matter with a senior team member and/or the engagement leader. The engagement leader may choose to seek advice from others in the Office such as other functional area specialists, including the Audit Services.

When applicable, the quality reviewer may be consulted; however, this consultation cannot compromise the quality reviewer's ability to perform his or her role and to make objective evaluations OAG Audit 3063 Quality reviewer responsibilities.

If there is still a difference of opinion, the engagement leader documents the issue giving rise to the difference of opinion and the opposing positions, including their rationale.

The issue will then move into Step 2—Arbitration, and the engagement report will not be dated until all differences of opinion have been resolved.

Differences of opinion between the engagement leader and the quality reviewer. On an engagement where a quality reviewer has been appointed, differences of opinion may arise between the engagement leader and the quality reviewer. For example, the quality reviewer may make recommendations that the engagement leader does not accept and the matter is not resolved to the quality reviewer’s satisfaction. If a disagreement cannot be resolved directly, the engagement leader documents the issue giving rise to the disagreement and the alternative positions, including their rationale, in the Differences of Opinion template. The issue will then move into Step 2—Arbitration, and the engagement report will not be dated until all differences of opinion have been resolved.

Step 2—Arbitration

If a disagreement cannot be resolved directly within the engagement team, the engagement leader shall escalate the matter according to the flow chart in the Differences of Opinion—Path to Resolution diagram in Figure 1.1. The Differences of Opinion template should be used to present a complete synopsis of the issue to the arbitrator(s).

Figure 1.1 Differences of Opinion (DofO)—Path to Resolution

When arbitration is needed, it is typically performed by a panel of individuals (this does not preclude a single individual acting from as arbitrator). A panel would normally comprise the assistant auditors general of the applicable audit practice and the assistant auditor general of Audit Services. Assistant auditors general acting to arbitrate a difference of opinion shall ensure any involvement in the audit engagement prior to or during the difference of opinion resolution process has not prejudiced their objectivity. This is an important prerequisite to an effective resolution process. Where needed, a panel arbitrating the difference of opinion resolution may involve outside experts such as assistant auditors general of other practices or members of the Office’s advisory committees and panels.

The arbitrators must consider the matter on a timely basis and meet with the parties involved, giving the arbitrators an opportunity to hear all parties' positions and to state their positions prior to making a determination. If the matter is complex or highly technical, the arbitrators will seek additional input as necessary. At the discretion of the arbitrators, advice may be sought from other functional area specialists, including Audit Services and others within or external to the Office.

Principles of arbitration:

-

The engagement leader assists the arbitrators by arranging and managing each consultation required during the arbitration process.

-

The individuals who have a difference of opinion shall attend all consultations required during the arbitration process.

-

The arbitrators will determine the factors to be used in reaching a decision and will communicate the decision to the parties involved.

-

The arbitration process may be completed at any point if all parties agree with the proposed resolution.

-

If the matter is resolved through arbitration, the engagement leader shall update the Differences of Opinion template to reflect the conclusions resulting from the arbitration process and the steps taken to implement the conclusion reached. The arbitrators shall review and agree to the documentation. This shall be documented on the Differences of Opinion template.

-

For each successive consultation that does not lead to a resolution, the Differences of Opinion template shall be updated to reflect the views of each of the consultations, the recommended courses of action, and why these courses of action were not considered appropriate in the circumstances.

-

The engagement report shall not be dated before all differences of opinion have been resolved.

If the difference of opinion cannot be resolved or if participants are not satisfied with the decision reached from the arbitration process, then the issue will move into Step 3—Appeal, for final resolution.

Step 3—Appeal

If there is dissatisfaction with the appropriateness of the arbitrators’ decision, either of the parties can make a final appeal to the Auditor General or an individual nominated by the Auditor General to hear the appeal and make a final determination. This step should be treated seriously and taken only where there is concern about a report being inappropriate in the circumstances or where there are concerns surrounding professional standards or other ethical matters that put the Office at significant risk.

The engagement leader shall provide the party hearing the appeal with the Differences of Opinion template, providing the synopsis of the issue and updated to reflect the views of all previous consultations.

The party hearing the appeal will

-

review the Differences of Opinion template which documents the agreed facts and the results of all previous consultations,

-

discuss the matter with the parties involved and others as considered necessary,

-

seek advice as required from within or external to the Office,

-

provide additional comments or argument, and

-

make a final determination.

The engagement leader is responsible for updating the Differences of Opinion template with the additional comments and arguments raised and the final determination made by the party hearing the appeal.

If a previous decision is overturned, the reasons will be communicated to all the parties involved and the engagement leader will update the Differences of Opinion template accordingly. The appeal process is the final recourse available within the Office.

Staff protection

The Office will protect employees from any form of reprisal, career limitation, or punitive actions for referring a legitimate matter of significance to the resolution of differences of opinion process in good faith and with the true interests of the public, the entity, the Office, or co-workers at heart.

1 Corporate knowledge = knowledge of past Office positions, interpretations, views, and conclusions on comparable situations.